This is the fifth of a 9-part series called the Founding Four, in which we dig deep about the four most important topics to tackle in your financial life. To get the most of this series, please read them in order.

Part 1 gave you an overview of all four principles and how they fit together. Part 2 explained the need to save for short-term needs, including an Emergency Fund. Part 3 explained how to save in a way that generated a better rate of return than a typical savings account. In Part 4, we discussed the various types of consumer debt, and explained briefly the difference between “smart” debt and meaningless, sabotaging debt.

As a means of quick review, as a financial planner, I don’t curse all debt as evil, but I don’t believe most of it is necessary, either. There is no such thing as “good” debt, but there is such a thing as “smart” debt.

“Smart” debt is debt that is taken on to either purchase an appreciating asset (such as a mortgage), or earns you more money in the long-term (such as a student loan). You can make bad decisions with otherwise “smart” debt, like taking 6 years to party through college and ending up with a worthless liberal arts degree, but generally, smart debt is something that will ultimately enhance your net worth or income for an extended period of time.

“Smart” debt is debt that is taken on to either purchase an appreciating asset (such as a mortgage), or earns you more money in the long-term (such as a student loan). You can make bad decisions with otherwise “smart” debt, like taking 6 years to party through college and ending up with a worthless liberal arts degree, but generally, smart debt is something that will ultimately enhance your net worth or income for an extended period of time.

That advice is really helpful for someone just getting started in life and doesn’t have a mountain of debt already, but what if you do? What if you already have the proverbial house, two cars, three credit cards, and the student loan? How do you get out of debt in a logical, meaningful way?

This part of our Founding Four will look similar to other financial pros’ advice, but I differ fundamentally from folks like Dave Ramsey on how to structure and pay down your debt.

Whereas Ramsey tells you, essentially, to strip away every luxury, subsist on beans and rice, and plow everything you earn into a debt paydown plan, I respectfully disagree. A draconian plan is a very hard one to stick with, and trying to balance your financial “stool” on just one fat leg doesn’t provide any sort of stability.

I believe you need to work on all of the Founding Four principles at the same time, not obsess about getting out of debt at the expense of building some short-term savings, insuring your family adequately against catastrophic loss, and taking advantage of compound interest for long-term investing.

You didn’t get into debt overnight, and you won’t get out of it overnight. And if you don’t save along with paying your debt down, you’ll have nowhere to go in an emergency except back to a credit card.

So to paraphrase the Greek historian Hesiod, let’s do all (four) things in moderation.

So how do you get a grip on your debt?

Like I said before, my advice is going to be similar to a lot of other gurus in this area, because it works. In fact, when you hear a lot of pros saying the same thing, a Rich Guy will heed their advice, and not try to be contradictory unless he has a very good reason. In my own experience as a planner, it’s always the guy who has virtually nothing that believes he’s an expert in everything. Rich Guys are not ego-led, deluded fools; they seek out expert advice and consider it carefully. (Hint: think like a Rich Guy.)

The very first step is to shut off the supply. I don’t mean to close your accounts, but you must commit, today, that you won’t go one penny further into debt of any kind, until you’ve eliminated what you have already.

Second, you must commit that you will never again take on debt for items that quickly depreciate in value. That means, no debt for appliances. No debt for clothing. I’m even hesitant to suggest debt for things like cars, which rapidly depreciate from the $40,000 you bought it for to $8,995 in 5 years.

Remember, Rich Guys use debt as leverage – as a means to actually grow their wealth, not as a means to acquire worthless stuff to look good to their friends and neighbors.

And finally, you have to commit to an organized, systematized plan to eliminate debt. That’s what the rest of this article will show you in detail – how to eliminate debt in one of the most recognized strategies of its kind anywhere: the “Debt Snowball”.

The Debt Snowball

As your virtual financial coach, I want you to work on your debts through a structured paydown plan commonly called the Debt Snowball.

I don’t know who coined the phrase, or who first invented the concept, but I’m a huge fan of this method of debt paydown. So are most financial experts. Why? Because it works.

If you’re unfamiliar with the debt snowball concept, it’s pretty simple:

- You make minimum payments on all of your debts except one. To that one, you add a certain about of extra. That’s the only debt that gets paid extra.

- Once that first debt is paid off, you move the entire payment you were making to that debt and add it to the minimum payment due on Debt #2.

As you pay off each debt, and move the entire payment on the previous debt to the next one on the list, the total amount you’re paying each month toward “debt” stays the same, but it rapidly begins to knock your later debts off because the monthly amount you’re paying gets applied more and more to a single debt. And that ever-increasing monthly payment on one debt at a time is where the strategy gets its name – it’s like a snowball that starts very small at the top of a hill, but gathers more snow and grows larger and larger as it rolls downhill.

You can pay off a lot of debt in an astonishingly short amount of time using this strategy.

Let’s see this in action in a hypothetical (but all-too-normal) situation:

(And I apologize in advance for the number of tables that are coming, but it’s important to point out specific data points and to watch the payment “snowball” as it pays debts off.)

Step 1: Gather your data

Let’s say we have as new clients a typical family with a 30-year mortgage, two 5-year car loans, a lingering student loan with 15 more years of payments, and three credit cards with balances. If I asked my client to simply list their debts, including the current balance due, the interest rate, and the minimum monthly payment for each, they’d come back with a list like this:

Pretty normal: $293,015 in total debt, with minimum monthly payments totally $2,630.

Step 2: Identify the really bad debt and any “smart” debt.

With this info, I would begin to determine in what order you should pay your debts down. You can see I’ve noted the highest interest rate debt with red, and added a column called “Tax Benefit” to note if any of this debt provides a tax deduction for the interest being paid.

Most American taxpayers get to deduct the interest paid on the mortgage of their primary residence and their qualified student loans. So even if you have these debts for a long period of time, at least the interest you’re paying comes back to you in the form of a tax write-off (assuming you itemize your deductions).

Step 3: Rank your debts in the order we want to pay them off

Generally speaking, you want to pay off the highest interest-rate debt first, and save the “smart” debt for last. In this case, the credit cards have to go first, no doubt. To pay 20% interest on a debt long-term is insanity. At 24%, for instance, your credit card balance will double every three years, even if you don’t charge any more purchases on it. You have to get rid of this high-interest debt as soon as possible, or you’ll be dealing with it for literally decades.

(By the way, credit card companies know this – that’s why the minimum payment due each month on most revolving credit is so low. There’s a reason the tallest building in every city is owned by a bank or an insurance company.)

So, after ranking these debts in the order from highest to lowest interest rate, with the “smart” debt at the bottom, our new paydown plan looks like this:

Step 4: Determine your plan’s “Extra” monthly payment amount

Obviously, you can’t get very far with a debt snowball if you don’t have a snowball to start with. You need to have a certain amount per month in addition to your minimum payments to start this process. It can be as little as $25 extra, but the more you can allocate, the faster this strategy takes off.

Let’s assume this family isn’t destitute and could cut some expenses or were willing to pick up a few nights working for Uber, and came up with an extra $370 a month. This brings their total amount of debt service from $2,630 a month to $3,000.

(I should also note, as we show you this “snowball” in rapid succession in the following charts, I’m not showing the slowly declining balances of the other debts as you make minimum payments on them. The point is to show you the paydown “snowball” in effect, not to be hyper-accurate with the figures in the scenario.)

Here’s how we start our Debt Snowball: we make minimum payments on all of our debts except the first one. That debt gets its minimum payment plus the extra $370.

Now our payment schedule looks like this:

Even at 28%, a $2,650 debt will be gone in approximately 7 months with this high of a monthly payment. (At $65, it would have taken in excess of 10 years to pay it off.)

Then, on that glorious month that you pay off your first debt, do you add the $65 a month back into your monthly budget?

NO.

Instead, you add the entire payment of the first debt (the entire $435) to the minimum payment on the next debt on your list:

Your second debt is now getting $475 a month (the original $40 due plus the entire payment from debt #1). With only $1,100 to pay off, this will take you only three months.

It’s been only nine months and you’ve already knocked down two debts totaling almost $4,000. And we’re just getting started:

Debt #3 gets $550 a month applied toward it instead of the $75 minimum payment. At that pace, even $3,125 is paid off in six months.

So we’re 15 months into this program and this family is already entirely out of credit card debt. And the best part is, the snowball is about to really pick up the pace on the larger debts still to go.

(I should add here that realistically, especially with installment debt like auto loans, 15 months of minimum payments would have dropped their balances due considerably. Just know this is a demonstration of the basic concept of the debt snowball, not a super-accuate accounting of the payment ammortization.)

As we begin to tackle the fourth debt, an auto loan, we add the entire previous payment “snowball” to the minimum monthly car payment of $225. We’re now paying $775 a month on that car.

At $775 a month, an $8,800 balance is paid off entirely in about 13 months. You’re barely two years into this plan, and you’ve eliminated almost $20,000 of debt.

But we’re not done yet. Add the $775 from the first car loan to the next one, and we’re paying $1,075 a month on car #2:

It will take just over 16 months to pay this debt off. Three and a half years into the plan, and all this family has left is a student loan and their mortgage.

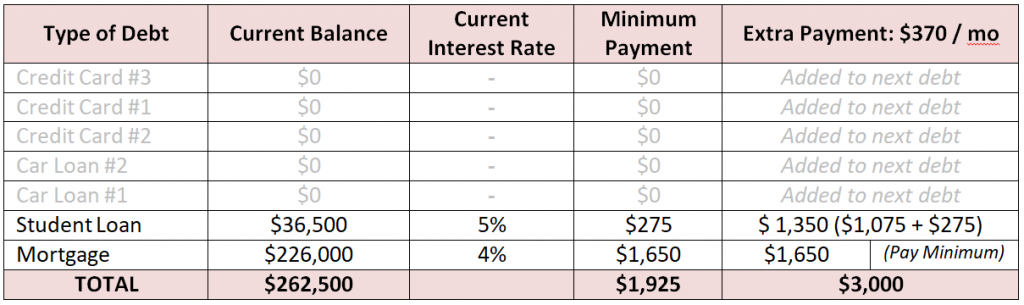

Now remember, we said the student loan still had 15 years of payments to go, and the mortgage was a typical 30-year loan. By moving the payment “snowball” down to the student loan, we’re now paying $1,350 a month on it instead of $275:

At $1,350 a month, a 15-year loan dwindles down to just about 2.5 years.

We’re six years into our plan, and this family has wiped out 3 credit cards, 2 auto loans, and a 15-year student loan. Now, all that’s left is the 30-year mortgage (with 24 years to go):

Making $3,000 a month payments on the last remaining debt, the home mortgage, changed it from 24 more years of payments down to just about 7 years.

I want you to think about that: almost $300,000 in debt, with payments extending out to 30 years for most of it, and it’s all entirely paid off in just under 14 years. This family is debt-free, including their home, in 14 years. Just by adding $370 a month, and “snowballing” the payments from one debt to another until everything is gone.

In this scenario, which is hypothetical but very typical, they saved 17 years of mortgage payments and over $100,000 in interest just on the home.

Your turn.

Would you like to become debt-free? It’s not going to happen magically, and it very rarely happens without a plan. The Debt Snowball is the fastest way I’ve observed for most families to eliminate debt in rapid succession.

Would you like to become debt-free? It’s not going to happen magically, and it very rarely happens without a plan. The Debt Snowball is the fastest way I’ve observed for most families to eliminate debt in rapid succession.

There are a lot of do-it-yourself methods out there for you to use, including this great calculator and spreadsheet.

However, you may find it all a bit overwhelming, or you feel out of your element. I understand that – that’s why I have my day job.

If you need mentoring on this or any other part of your Founding Four, feel free to ask me for some one-on-one time (free of charge). It’s yours for the asking – simply schedule a 15-minute call with me here.

If you’ve had success with the Debt Snowball, or any other debt payoff strategy, I’d love to hear your story! Reply here in the comments, or shoot me a personal email to jeremy@thinklikearichguy.com.

The next two weeks, we’re delving into the confusing, sketchy but important world of insurance: different types, what’s a ripoff, what your family needs, and where I’d advise you to get quotes.